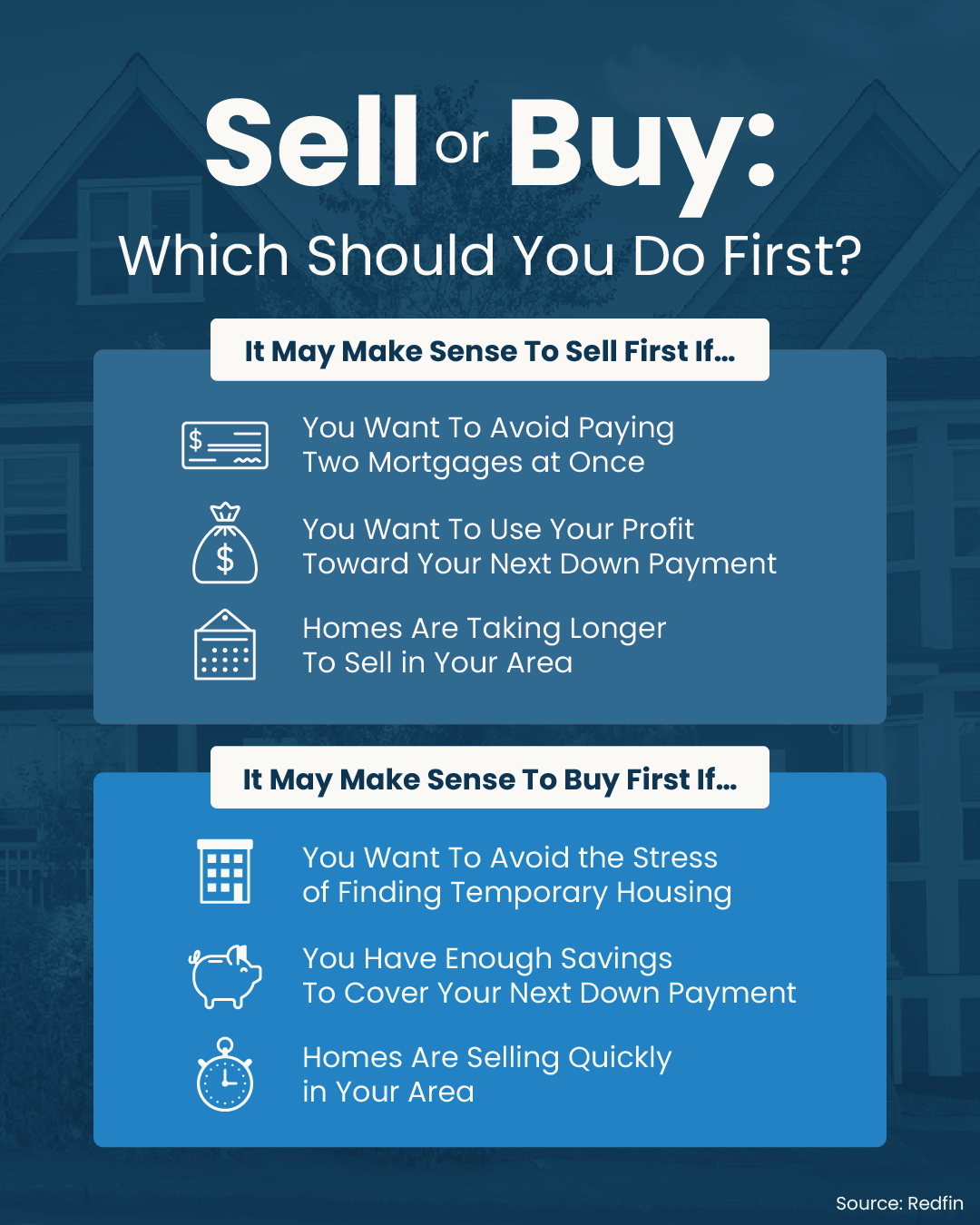

When planning a move, one of the most consequential decisions homeowners face is whether to buy their next home first or sell their current home first. Both routes come with distinct financial, logistical, and emotional implications, and the right decision often depends on a blend of market conditions, personal financial standing, and risk tolerance.

Selling First: A Conservative Yet Strategic Approach

For many homeowners, the default strategy—particularly in a buyer’s market or when financial flexibility is limited—is to sell their current home first. This approach minimizes financial risk by ensuring that the sale proceeds are in hand before committing to a new purchase. According to Realtor.com, this strategy is especially appealing for homeowners who need the equity from their current home to fund the down payment on their next one. Selling first also enables buyers to better understand their purchasing power without the burden of juggling two mortgages.

The biggest advantage of selling first lies in financial clarity. The National Association of REALTORS® emphasizes that selling before buying helps eliminate contingency complications and reduces the chance of being forced to accept less-than-ideal financing options. In addition, homeowners who sell first are in a stronger position to negotiate with prospective buyers, especially when they are not under pressure to quickly accept an offer to make a subsequent purchase viable.

However, selling first comes with its own set of challenges, most notably the potential disruption of temporary housing. Unless you can align the closing dates of your sale and purchase perfectly—a feat rarely accomplished you may need to rent for a short period or move in with friends or family. There also may be additional costs associated with double moves, temporary housing, and storage fees that can erode the financial benefits of selling first, particularly if you stay in the interim home for more than a few months.

Additionally, timing the market can be difficult. Homeowners risk selling during a market dip and may then be priced out if the market rebounds quickly. Even a small uptick in prices or interest rates between transactions can significantly impact affordability and home availability.

Buying First: Ideal for Competitive Markets and Confident Financers

On the flip side, buying a new home before selling your current one offers continuity and comfort—two factors that weigh heavily for families with children or those who prefer to avoid temporary living situations. In a fast-moving seller’s market, where homes receive multiple offers within days, acting quickly is often essential. Buyers who are not contingent on selling their current home are more competitive in bidding wars and can often close faster, making them more attractive to sellers.

One of the most practical benefits of buying first is that it allows you to move at your own pace. You can stage your old home more effectively for sale without the clutter and chaos of daily life. This can result in a higher sale price, as staged homes tend to sell faster and at better prices than occupied ones. Moreover, you avoid the double move, which can be particularly taxing both financially and emotionally.

But buying first comes with financial risks that not all homeowners are prepared to shoulder. Carrying two mortgages simultaneously—even for a short duration—can strain monthly budgets. Realtor.com recommends that only homeowners with substantial savings or a high debt-to-income tolerance consider this route. Additionally, there’s always the risk that the original home takes longer to sell than anticipated or sells for less than expected, creating liquidity issues or even forcing a discount sale.

Bridge loans or home equity lines of credit (HELOCs) can provide temporary liquidity, but these come with their own caveats. Bridge loans tend to carry higher interest rates and stricter qualification criteria. If your home doesn’t sell quickly, the interest payments on a bridge loan can accumulate rapidly, eroding any financial advantage gained from buying first.

Market Conditions: The Deciding Factor

Understanding current market dynamics is crucial. In a seller’s market—characterized by low inventory and high demand—it’s often safer to buy first. In a buyer’s market, where inventory is high and demand is lower, selling first is generally advisable. Seasonal trends also matter. Spring and early summer are typically the hottest times to sell, while winter often yields better purchase opportunities due to less competition.