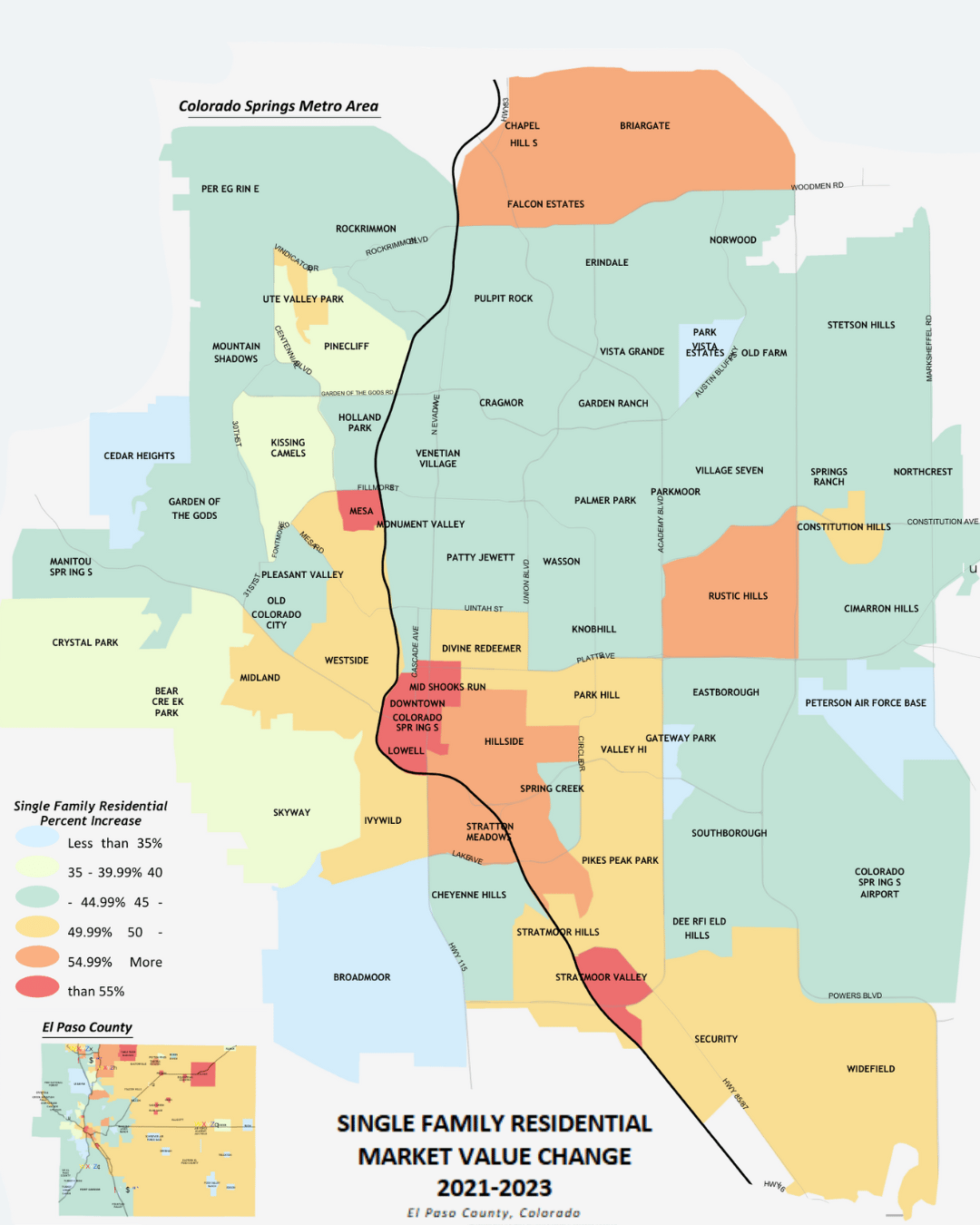

Understanding Your 2025 Property Valuation

- 06/2/25

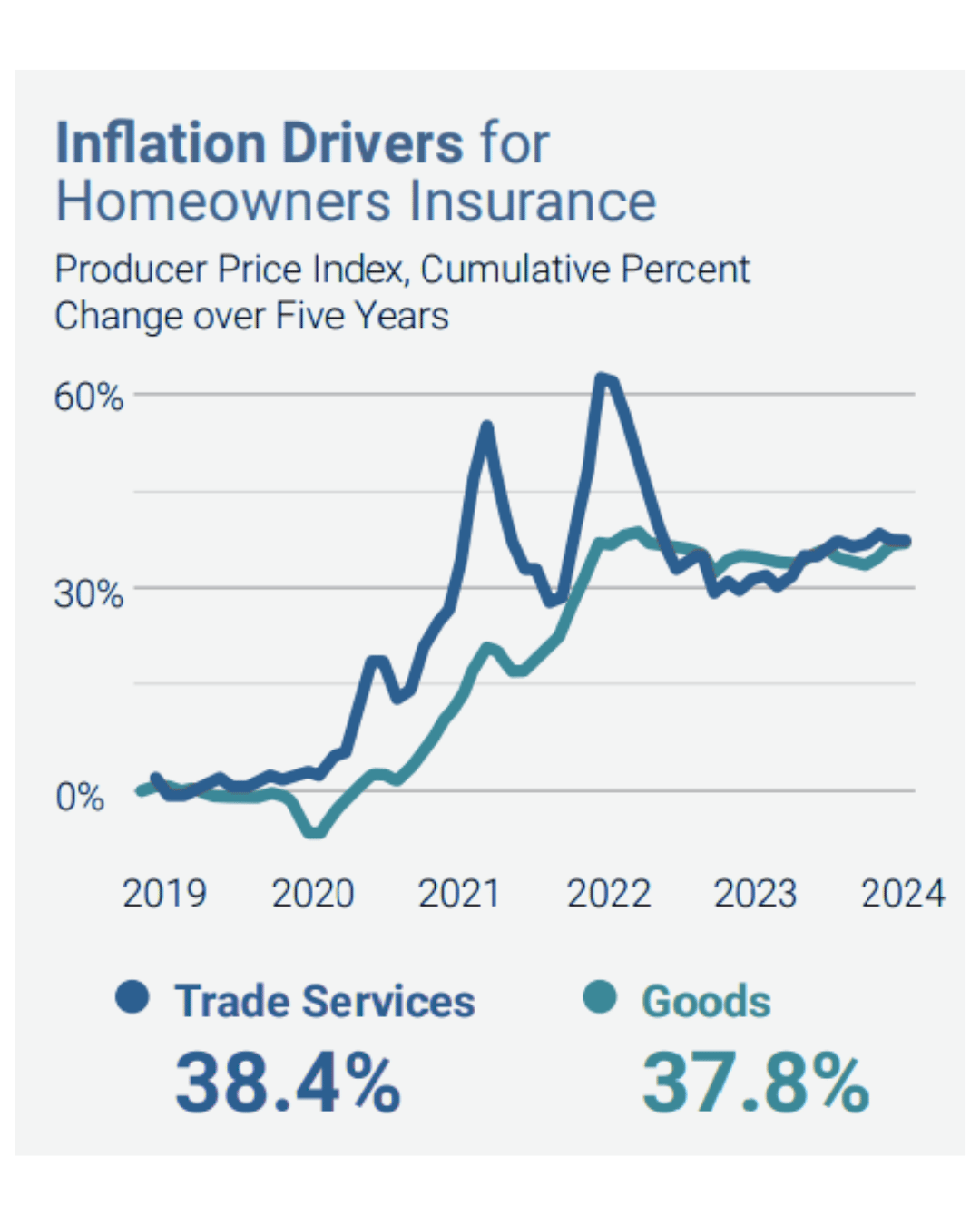

Colorado Ahead of Nation in Homeowners’ Insurance Hikes

- 05/1/25

ADUs Are Hot Item Among Today's Homebuyers

- 04/1/25

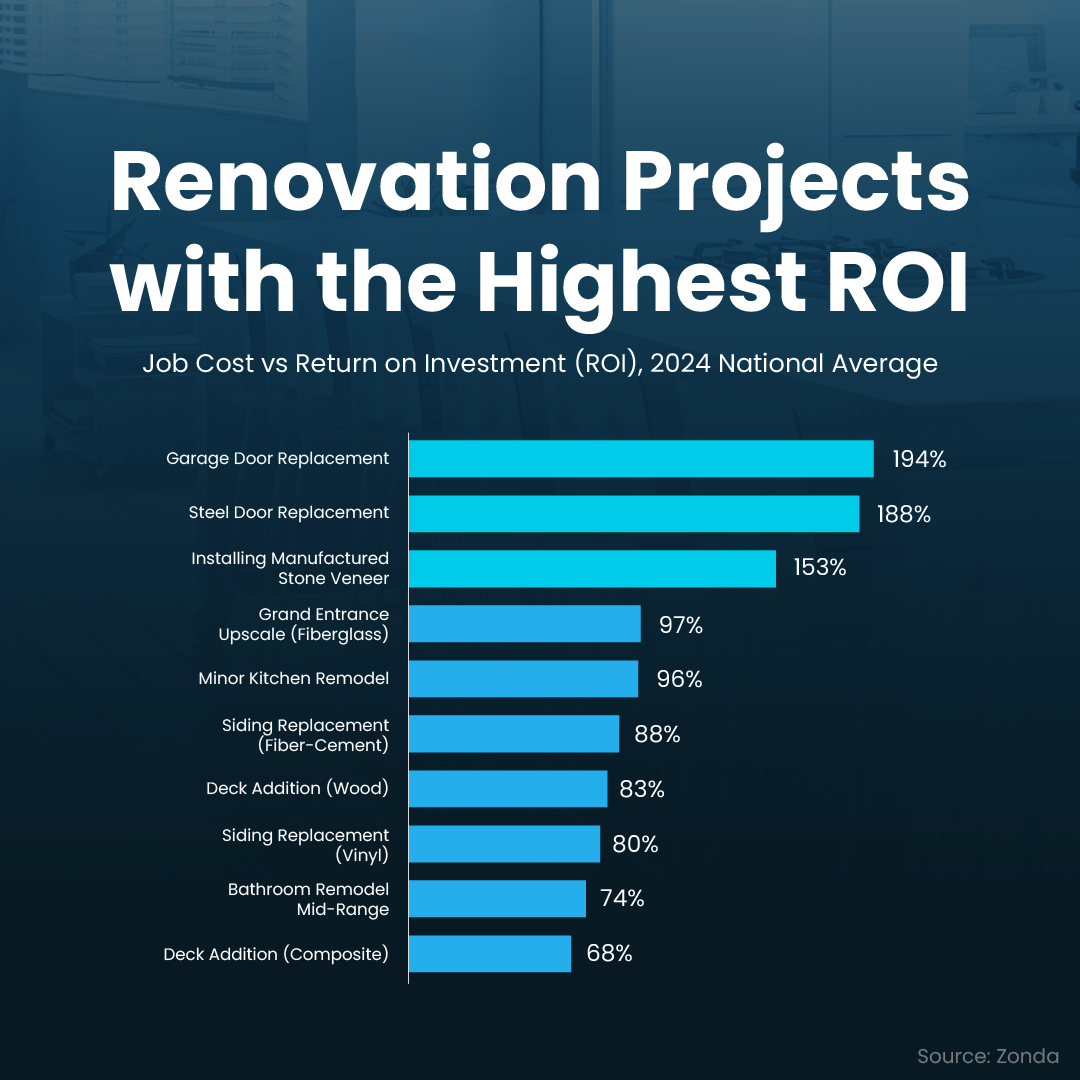

Prepare for Spring Home Sale With Key Repairs, Exterior Upgrades, Quick Wins

- 03/1/25

A Challenging Home Buying Season

- The Platinum Group

- 05/3/23

The continuing low inventory and rock-bottom mortgage rates would set the stage for a competitive spring buying season.

Read MORE

8 Tips to Keep Your Home-For-Sale Cozy This Winter

- The Platinum Group

- 05/3/23

Making sure your home withstands the snow, wind and cold is vital in keeping the inside warm and cozy for your family.

Read MORESorry, we couldn't find any results that match that search. Try another search.