Condo Sales Face Challenging Headwinds

- 07/1/25

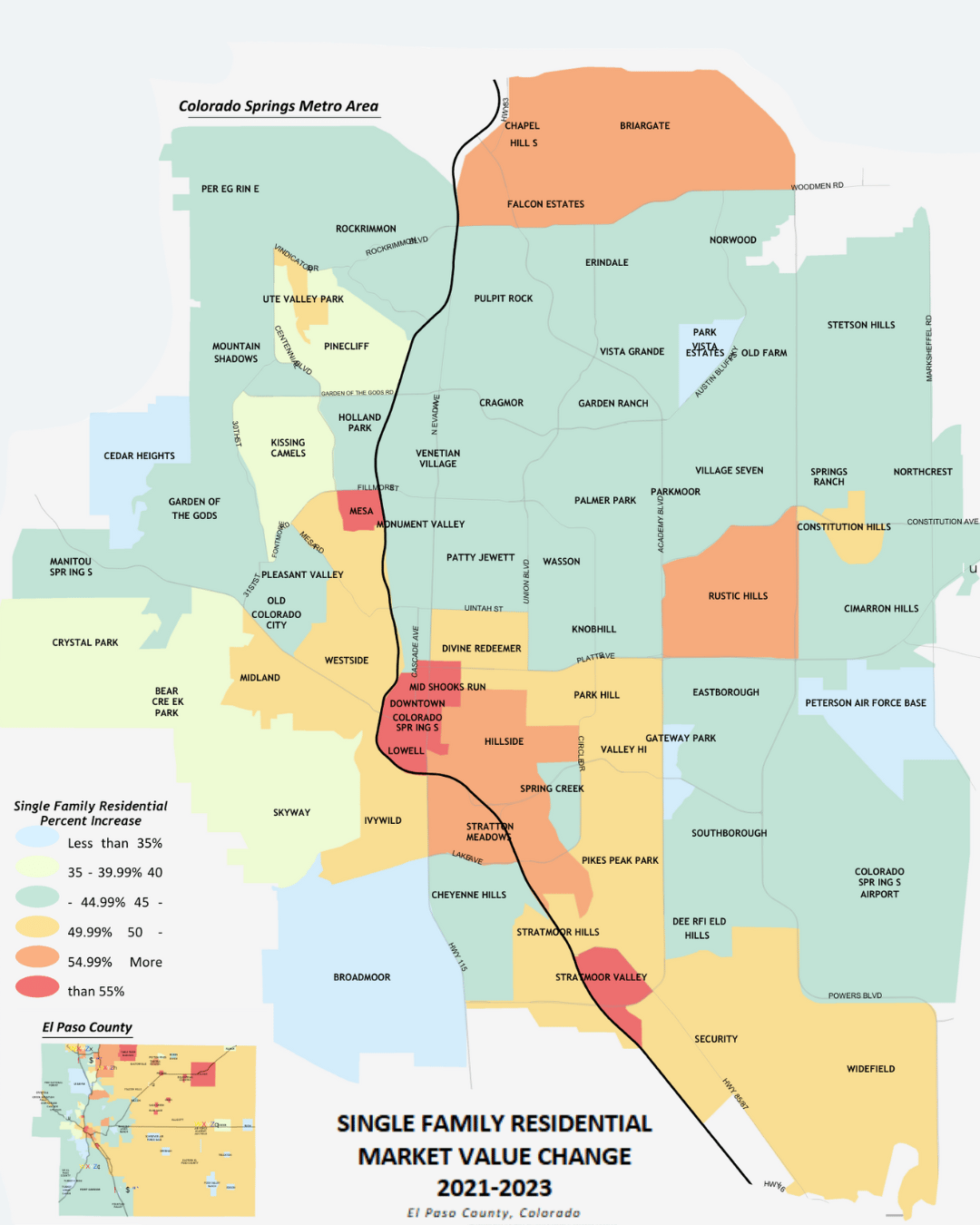

Understanding Your 2025 Property Valuation

- 06/2/25

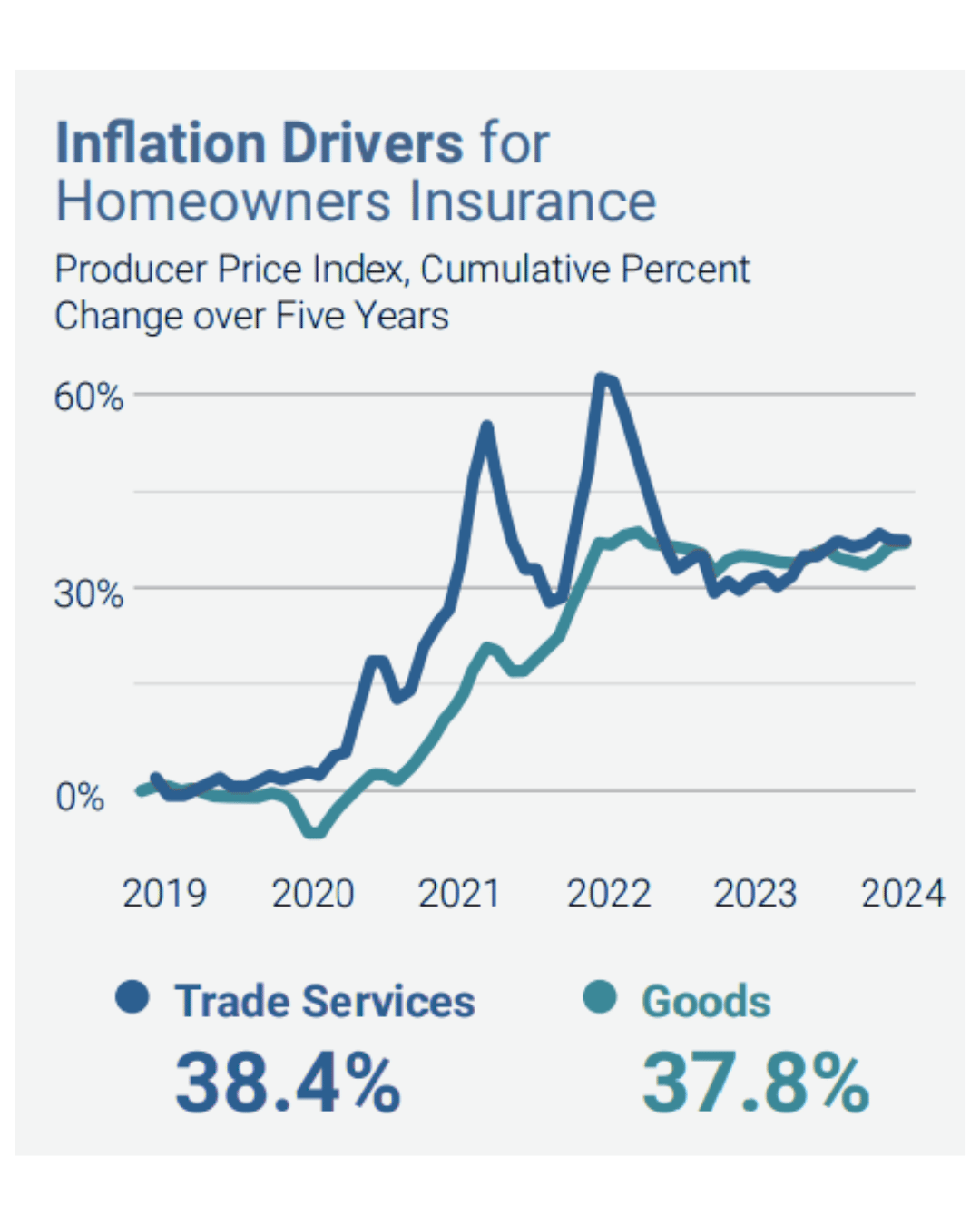

Colorado Ahead of Nation in Homeowners’ Insurance Hikes

- 05/1/25

ADUs Are Hot Item Among Today's Homebuyers

- 04/1/25

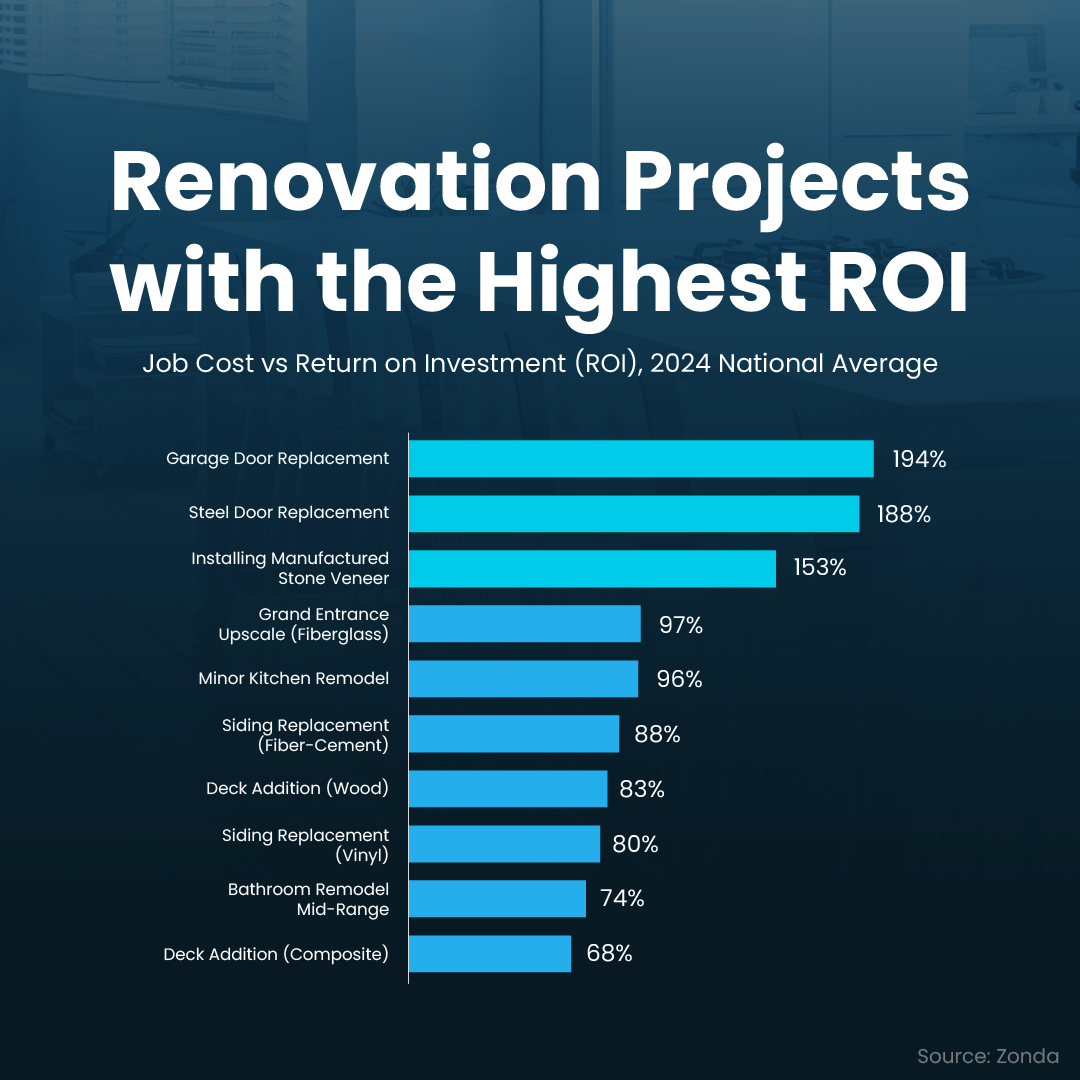

Prepare for Spring Home Sale With Key Repairs, Exterior Upgrades, Quick Wins

- 03/1/25

A Challenging Home Buying Season

- The Platinum Group

- 05/3/23

The continuing low inventory and rock-bottom mortgage rates would set the stage for a competitive spring buying season.

Read MORESorry, we couldn't find any results that match that search. Try another search.