Buying a second home, if done with careful financial planning, can be a strategic and rewarding move for your future retirement. While many people think of retirement planning primarily in terms of savings accounts, pensions, or investment portfolios, real estate—particularly a second property—can play a unique and powerful role in building long-term wealth, creating passive income, and enhancing your lifestyle.

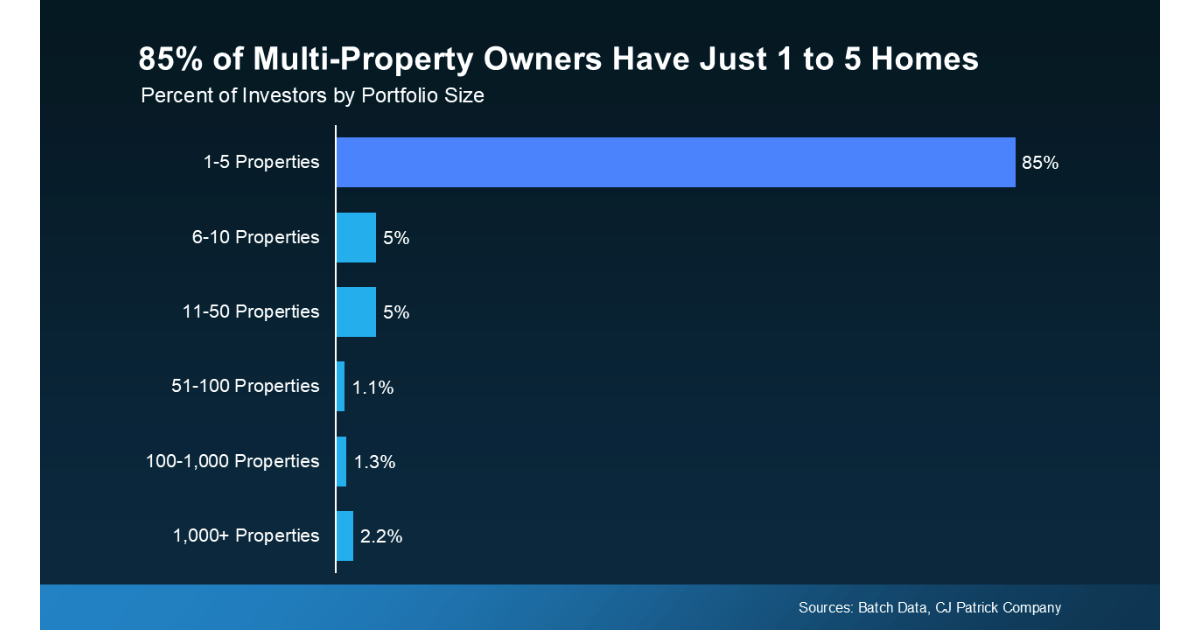

And if you’re thinking: wait, owning multiple homes is only for big investors – data shows that's not necessarily true. Data from real estate platform BatchData, 85 percent of people who own more than one property have just 1 to 5 homes. That means most who own multiple homes are people (not large investors) who’ve bought an extra home to rent out or hold onto for later.

One of the main advantages of purchasing a second home is the potential for asset appreciation. Real estate historically trends upward in value over the long term, especially in desirable areas such as coastal towns, mountain regions, or growing metropolitan suburbs. By buying a property now, you lock in today’s prices while allowing time and market conditions to work in your favor. When retirement arrives, you could sell the property for a profit, downsize, or use the equity to fund your lifestyle.

A second home can also generate rental income, which can become a vital supplement to retirement savings. In the years before you stop working, you could rent the property short-term (via platforms like Airbnb or Vrbo) or long-term to consistent tenants. This income can offset mortgage payments, property taxes, and maintenance costs—sometimes even turning a profit before you retire. By the time you reach retirement, you may own the home outright, giving you a steady income stream without the burden of a monthly mortgage.

Tax benefits are another often-overlooked reason a second home can be a smart investment. Depending on how you use it, you may be able to deduct mortgage interest, property taxes, and certain expenses related to maintenance or rental management. If the home is primarily a rental property, you could also benefit from depreciation deductions, which can reduce taxable income. While it’s important to consult a tax advisor for specifics, the financial advantages can be significant.

Beyond the dollars-and-cents perspective, a second home can offer lifestyle benefits that enhance your retirement years. Imagine having a familiar, comfortable retreat where you already know the community, neighbors, and amenities. Whether it’s a mountain cabin, beachfront condo, or city apartment, your second home could serve as a ready-made vacation spot during your working years and a primary residence in retirement. This eliminates the stress of finding a new home later in life and gives you years to create memories with friends and family in the same place.

A second home can also serve as a hedge against housing market uncertainty in your retirement location. If your primary residence is in an area where costs rise significantly, you have the option to downsize into your second home or relocate entirely, giving you financial flexibility and control over your living situation.

Of course, making the numbers work is essential. That means considering mortgage affordability, maintenance costs, insurance, and taxes, as well as realistic rental income projections if you plan to rent it out. When purchased strategically and with a clear plan, a second home isn’t just a luxury—it’s an investment in your future comfort, financial security, and peace of mind.

In short, if you can align the financial pieces, buying a second home now can give you both tangible assets and lifestyle freedom later. It’s a move that can pay dividends—both in your bank account and in your quality of life—long after you’ve stopped working.